Skip to content

Skip to content

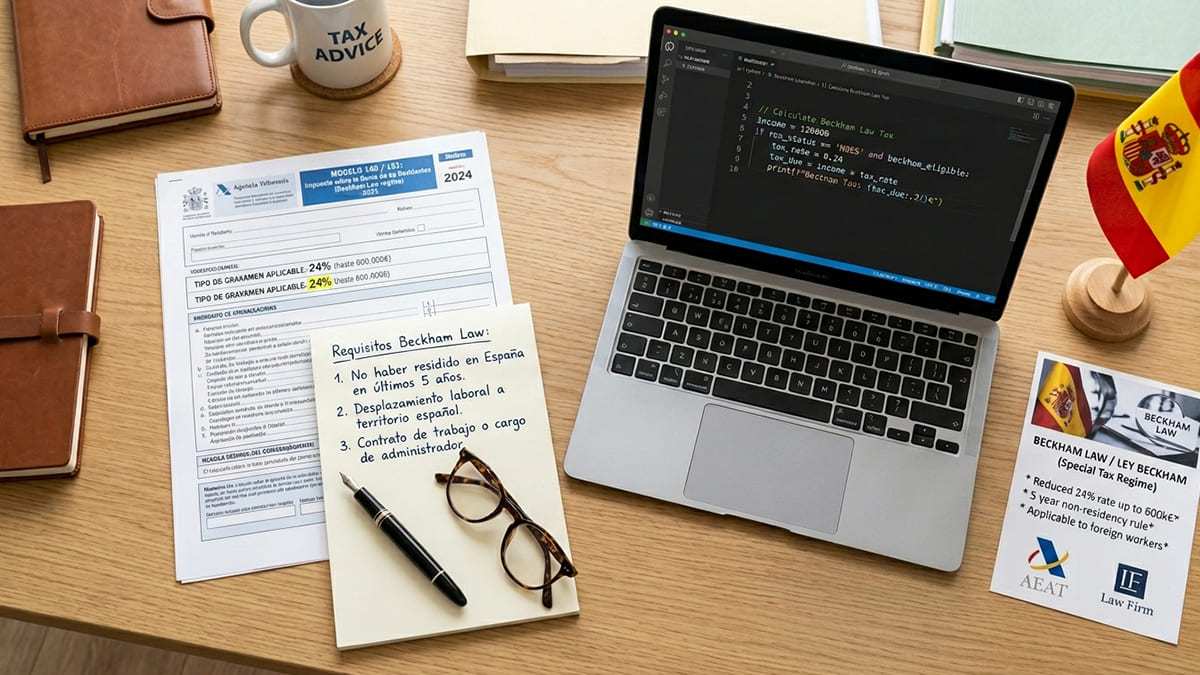

Situation

The IT developer registered as an autónomo in Spain. Was paying IRPF up to 47%; effective burden: 43%. Earned 80%+ from foreign clients (Netherlands, UK). Important 2026 clarification: a standard autónomo primarily serving Spanish clients does NOT qualify for the Beckham Regime (Art. 93 LIRPF). Following the Law 28/2022 reform, eligibility requires three conditions simultaneously: (1) a Digital Nomad Visa or other Law 28/2022 permit, (2) ≥80% of income from foreign clients, (3) no permanent establishment in Spain.

Solution

Our lawyers confirmed all three conditions were met: Spanish tax residence less than 5 years, 80%+ income from foreign companies, no PE in Spain. A Digital Nomad Visa was obtained. Modelo 149 was filed with the AEAT within 6 months of Social Security registration. Lawful expense accounting (home office, equipment, training, subscriptions) and quarterly filings (Modelo 130, 303) were simultaneously optimised.

Result

Beckham Regime applied: effective IRPF reduced from 43% to a flat 24% for 6 years (up to €600,000 of income). Additional lawful deductions ~€9,200/year. Total first-year savings: over €21,000.